Popularly known as ESOP, is an employee benefit that offers them an ownership interest in the organisation. This employee stock ownership plan is intended to encourage the involvement of employees in the company by giving them the right to acquire stocks in the company.

The employer of a company gives certain stocks of the company to the employee for negligible or no cost. The stocks remain in the ESOP trust fund until the option vests and the employee exercises the same or the employee leaves/retires from the company or organisation. The goal is to increase the value of the shares by involving stockholders who are employees of the company. This eventually helps in resolving issues related to incentives.

You must have come across many examples where the employees became rich by selling their ESOP. It is a quite known pattern now, especially in the case of IT companies and Startups. Flipkart was India’s largest ESOP pool, valued at Rs. 17,000 crore.

ESOPs are issued as direct stock, profit-sharing plans, or bonuses, and the employer has the right to decide who could avail of these options as the plan is spread over a period of time known as the vesting period. These options can be purchased at a specified price before the exercise date.

There are rules and regulations pertaining to granting of ESOP by companies to their employees. We shall discuss the various aspects affecting the Employees Stock Option Plans in this article especially those related to taxation.

The Mechanism of ESOPs

When a company grants ESOPs to its employees for buying a specified number of shares at a defined price after the option period, the employee should understand how much the pre-defined vesting period is. To exercise the stock option either partly or fully, the employees have to work for the company.

This helps the company to retain highly qualified employees. Stocks are normally distributed by companies in a phased manner and until then this works as an incentive for working with the organisation. The company gets a long-term involvement of their staff in return. Many IT companies have adopted this practice as they do not offer handsome salaries but instead make the compensation package attractive by choosing ESOPs.

The employees at the same time get the benefit of acquiring the shares of the company at a nominal rate. By selling them, they can book profits. ESOPs may lead to genuine wealth creation. Workers and other skilled paid staff are understanding the importance of ESOP as salary hikes are not enough to bring any remarkable change in their lifestyles.

It should be noted that the company does not charge anything at the time of offering ESOPs to employees just that to exercise this option, a certain lock-in period applies. Usually it is more than one year. The right to exercise ESOP may get vested in the employee in the future dates. The dates on which the employees become entitled to exercise the right to acquire the shares is called “vesting date”.

For example, On April 1st 2018, ABC India Private Limited granted ESOP to its employee Mr. X to purchase 1000 shares at a predetermined price of Rs. 100 per share. The date of vesting of ESOP is April, 2021. He can exercise the right to purchase shares on or after April 1st, 2021.The employee is given a time period during which he has to exercise and failure to do so will result in lapse of such rights. The date on which the employees exercise this option to buy the shares is known as ‘exercise date’.

It should be noted that in the case of ESOP, employees are given an option to exercise such an option, and it is not mandatory for them to exercise such ESOP.

Taxation of ESOP

Well, this is one of the most crucial areas that one needs to be aware of as an employee who has been offered the ESOP.

The tax treatment has been explained here.

- At the time of allotment of shares-as a perquisite : Any company that is responsible for paying salaries to employees shall deduct tax at the time of payment of such salary at the average rate of tax. The perquisites are also part of the salary. The value of any share allotted would be treated as a perquisite, irrespective of them being offered free of cost or at a concessional rate.It will be included under the head, ‘Income from Salary’ in the Income Tax Return.

The employee who is offered an ESOP, decides to exercise the option, or agrees to buy; the difference between the FMV on exercise date and exercise price is taxed as perquisite. The amount paid by the employee is taxable as a perquisite.Though the tax is levied at the time of allotment of shares but the

FMV of shares at the time of exercising of option is considered for calculating the value of perquisite and not the FMV of shares at the time of allotment of shares. TDS is deducted by the employer on it and the amount is shown in the employee’s Form 16.

FMV=fair market value

Exercise price=The price at which employee exercises the option. The price is lower than the prevailing FMV.

Because of the amendment made in the rules in 2020, from the FY 2020-21 onwards, an employee receiving ESOPs from an eligible startup need not pay tax in the year of exercising the option. The TDS shall also stand deferred to earlier of the following events:

- Expiry of five years from the year of allotment of ESOPs

- Date of sale of the ESOPs by the employee

- Date of termination of employment.

(This has been discussed later in this article)

The following steps can be useful in calculating tax in this situation:

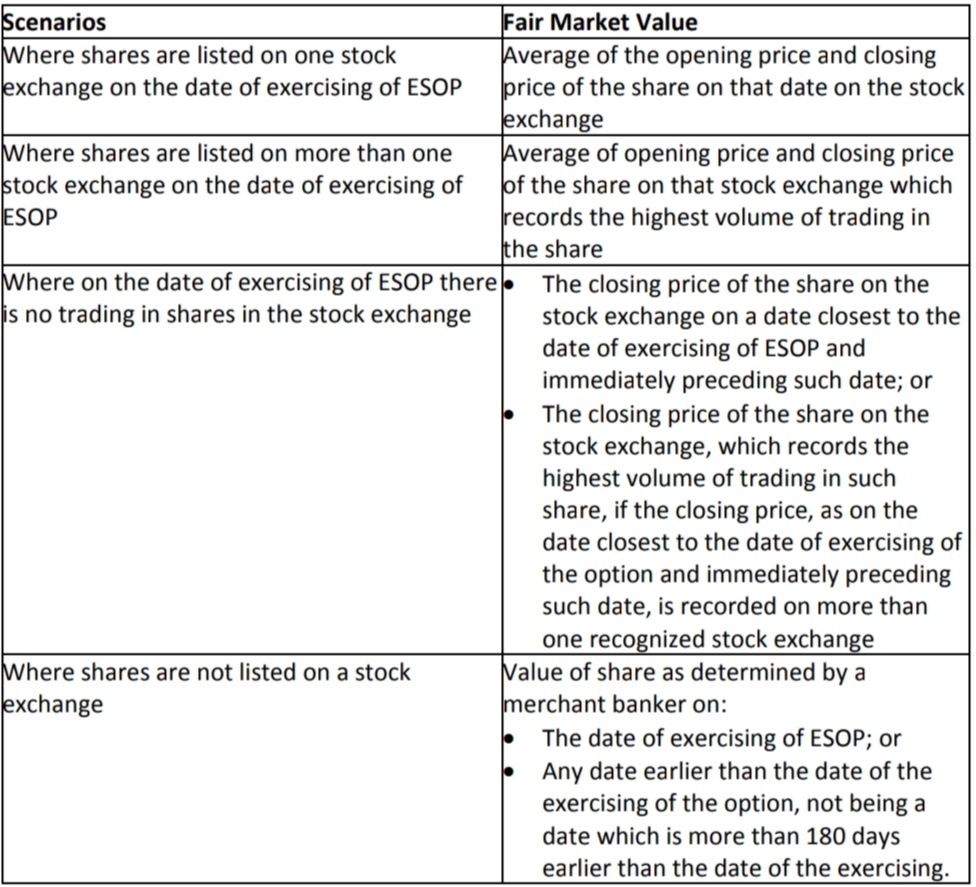

Step 1. Determine the Fair Market Value of shares on the date on which the employee exercised the option. Note that the FMV of shares on the date of vesting shall not be considered.

The FMV of any specified security, not being an equity share in a company, on the date on which the option is exercised by the employee, shall be such value as determined by a merchant banker on-

- The date of exercising of the topion or,

- Any date earlier than the date of exercise of option, not being a date which is more than 180 days than the date of the exercising.

Step 2. Take the predetermined value of shares paid or to be paid by the employee to the employer at the time of exercising of option.

Step 3. Value of perquisite=(Step 1 Minus Step 2) x Number of shares exercised by the employee.

- At the time of sale by the employee-to be taxed as a capital gain: After buying the shares, an employee may choose to sell them. The difference between the sale price and FMV on the exercise date is taxed as capital gains.

Here is an example to explain the above two instances.

On 1st April 2021, Ankur joined a company and he had the option to purchase 500 shares at an exercise price of Rs. 300 per share. The vesting period is 20% at the end of each year of service in the company. On the said date, the market value of the company’s share is Rs. 800 per share and Ankur decides to buy 100 shares. He pays Rs. 30,000. The difference between the exercise price and market price Rs. 50,000( Rs.500 X 100 shares) shall be taxed as a perquisite in his hands. TDS will be deducted by the employer on this amount. As long as this option vests and Ankur opts for the same by purchasing shares, a similar kind of tax treatment is applicable.

Now on 1st June 2024, Ankur sells 100 shares for Rs. 1000 per share, the long term capital gains tax shall be payable on Rs.20,000 (Rs.1000-Rs.800).

Let’s take another example to understand the capital gains on ESOP.

Mr. Z exercised ESOP on 1st April, 2018 and the shares were allotted to him on 1st May 2018. He sold shares on 1st April 2020. The period of holding of these shares shall be considered from 1st May 2018 and not 1st April, 2018 till 31st March 2020. But for calculation purposes, the cost of acquisition as on 1st April,2018 shall be taken into account.

The computation of capital gains shall be done in the following manner for listed and unlisted shares-

Listed equity shares

Long-term capital assets: When the allotted shares are equity shares, and the employee sells them after holding for more than 12 months, the long term capital gains resulting therefrom shall be taxable under section 112A. The period of holding shall be counted from the date of allotment of shares to employees under ESOP. The long term capital gains to the extent it exceeds Rs. 1 lakh shall be taxable at the concessional rate of 10%.

Short-term capital assets: Short-term capital gains arising from the sale of listed equity shares allotted under ESOP shall be liable to tax at the rate of 15% u/s 111A.

Unlisted equity shares

Long-term capital assets: If an employee sells unlisted shares after holding for a period of more than 24 months, the long term capital gains thus arising will be taxable at the rate of 20% under section 112. Period of holding of such shares shall be counted from the date of shares to employees under ESOP.

Short-term capital assets:Any short term capital gains arising from the sale of unlisted equity shares shall be taxable as per the Income-tax slab rate applicable to the taxpayer.

The Fair Market Value of shares on the date of exercise of ESOP shall be computed as shown in the table below.

Example for calculating the value of perquisite: Mrs. A is working with a private limited company. She was given ESOP on 1st June 2018 to purchase 1000 shares at a price of Rs. 500 per share.

The vesting period being 1-06-2018 to 31-03-2020. She exercised the option on 31-03-2020. FMV on that date was Rs. 5000 on NSE and Rs.5500 on BSE. The BSE recorded the highest volume of trading in such shares.

The company allotted shares to her on 30-04-2020. The FMV on the date of allotment was Rs.4000 on NSE and Rs.4500 on BSE.The NSE recorded the highest volume of transaction on that date.

The value of perquisite value shall be considered on bases of FMV on 31-03-2020 and will be taxable in the financial year 2020-21 because the FMV of shares on the date of exercise of option is considered for valuation of perquisite and it is taxable in the financial year in which shares get allotted. Note that since shares are listed on more than one stock exchange, the FMV shall be the price of shares on the stock exchange which records the highest volume of transaction.

Value of perquisite=Rs.50,00,000(Rs.5500-Rs.500)x1000

Taxability of ESOPs in case of startups

As ESOPs often play an important role in the journey of startup companies, let’s understand how tax rules apply in case of startups.

The tax liability arises in the hands of employees at two instances. Firstly, when shares are allotted to employees on exercising his right to apply for shares under ESOPs and secondly, when such shares are sold by the employee.

At the time of allotment of shares: Under section 17(2)(vii) of the Income Tax act, the difference between the FMV of shares on the date of exercising the option and the amount actually paid by the employee for such shares is taxable under the head Salary. The employee will deduct tax on it u/s192 in the year in which shares are allotted.

The Finance Bill 2020 introduced some relaxation on taxation of perquisites on ESOPs issued by start-ups. Section 192 was amended(TDS on salary), Section 140A(self-assessment tax), Section191(direct payment of tax by the employee) and Section 156(notice of demand)so to defer the deduction and payment of tax on income in the nature of perquisites arising from ESOPs for eligible startups as referred to in section 80-IAC.These relaxations are available if the start-up:

1. Was incorporated between 1 April 2016 and 31 March 2023 [as amended by finance bill 2022]

2. Has total turnover of less than Rs.100 crores for the year in which benefit is sought.

3. Is certified as an eligible start-up by the inter-ministerial Board of the Government of India.

An eligible startup shall deduct tax from income arising in the nature of perquisites from ESOPs within 14 days from the happening for the following events(whichever is earlier):

a) Expiry of 48 months from the end of the relevant assessment year (AY); or

b) From the date of sale of such ESOP shares by the assessee; or

c) From the date of the taxpayer ceasing to be the employee of the ESOP allotting employer

The rates of tax in such cases shall be the one applicable for the year in which ESOP was allotted.

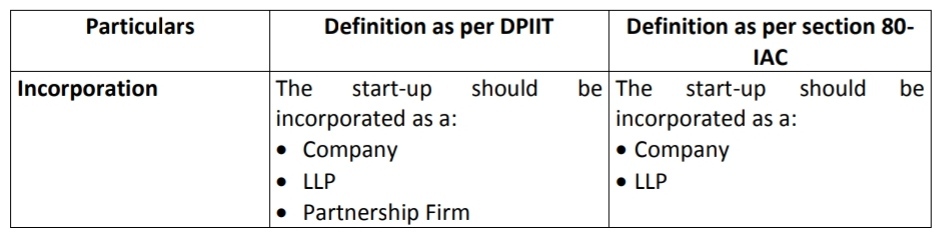

What is an eligible startup?

An eligible startup referred to in Section 80-IAC and its employees would get the benefit of deferment of TDS and tax payment on perquisites arising from ESOPs. Accordingly, an eligible startup can only be a company or limited liability partnership engaged in innovation, development or improvement of products or processes or services or a scalable business model with a high potential of employment generation or wealth creation.

The table below explains the definition in a different manner given by DPIIT.

We will study the effect of the above provisions with the help of an example, company PQR is an eligible start-up fulfilling all conditions stated above. Mr.Y joined the company on 1 April 2021 and had the option to purchase 5,000 shares at an exercise price of Rs.10 per share. The vesting period is 20% at the end of each year of service. Suppose the fair market value of the company’s shares is RS.100 per share. Mr. Y exercises the option to purchase these shares and pays an amount of Rs.10,000 [ Rs. 10 x1000 shares].

The difference between the exercise price and the fair market value=Rs.90,000(Rs.90per share x 1,000 shares) will be treated as a perquisite in the hands of Mr Y. However, the tax on such perquisites will not be immediately payable and hence the employer will not have to deduct TDS on the same.

Assuming three different scenarios,

Scenario (a): Mr.Y continues as an employee of the company and holds the shares. The shares were purchased in FY 2022-23 (AY 2023-24) and hence tax will be due at the expiry of 48 months from AY 2023-24 i.e. 31 March 2028. The tax will be payable by him within 14 days i.e. 14 April 2028.

Scenario (b):He sold the shares on 30 June 2023. Tax on perquisite will be payable by him within 14 days. There is no change in the taxation of LTCG on sale of shares obtained under ESOP.

Scenario (c) : Mr.Y ceases to be an employee of the company on 31 May 2023. Then the tax will be payable by him within 14 days.

In all three scenarios, the tax rate applicable on the perquisite amount of Rs.90,000 will be the applicable tax rate for AY 2023-24.

ESOPs are part of a remuneration package, and are chargeable to tax. Employees need to consider the net benefit post the tax outgo if ESOPs are included in their salary package.

Deferment of tax on perquisite arising from ESOPs

As there is no amendment made to section 17(2)(vii) despite the Government providing for the dergerment of tax and TDS on perquisite arising from ESOPs, the perquisite shall be treated as income of the employee of the year in which the shares are allotted but no tax would be deducted or paid by the employer and the employee. It shall be included under the head ‘Salary’.The employee shall disclose the value of it in his return of income of the year in which shares are allotted. The employee shall not be required to pay the perquisite arising from ESOPs in such year. The tax to be payable on the salary income, excluding the perquisite value or ESOP, will be computed as per the following formula:

Tax payable on salary income excluding ESOPs perquisite=Tax on total income including ESOPs perquisites X Total income excluding ESOPs perquisites/Total income including ESOPs perquisites

Example:An employee is allotted 1 lakh shares at the rate of Rs.10 per share under ESOP

Financial year:2020-21. FMV at the time of exercising of option is Rs.100.

Value of perquisite=Rs.90 lakhs(Rs.100-Rs.10)x1 lakh shares. Let’s further assume that the salary of the employee is Rs. 40 lakhs excluding the value of the perquisite of ESOPs. The employment is continued after expiry of 48 months from the end of the assessment year in which shares are allotted and the shares are not sold after the aforesaid period. The deferment of TDS and tax on perquisite value of ESOPs shall be as under:

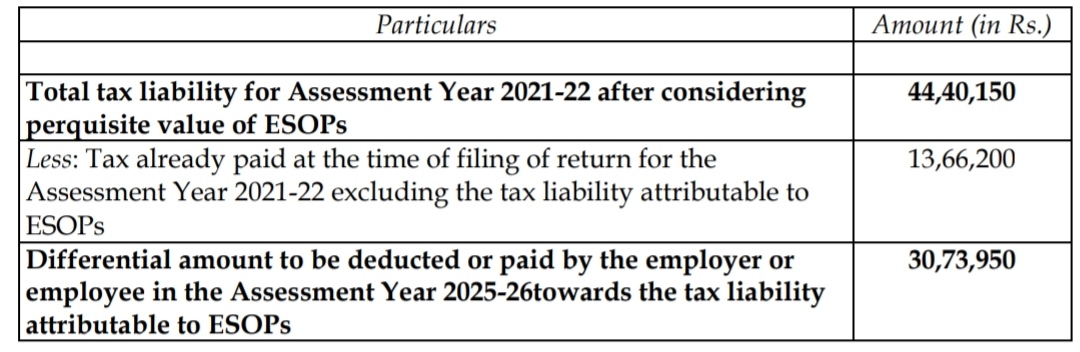

Assessment Year 2021-22

Note that Rs. 90 lakh are included in his ITR but tax shall not be paid in the year of allotment of shares. Tax is paid excluding the perquisite value of ESOPs.

Assessment Year 2025-26

The liability to deduct tax or make payment of tax on the perquisite value of ESOP will arise in the A.Y 2025-26 or 48 months from the end of the A.Y 2021-22.

What happens in case of failure to deduct/pay tax on perquisite value of ESOPs:

Where a person who was liable to deduct tax at source fails to do so or after deducting fails to pay such tax to the central government, he shall be deemed as assessee-in-default. The assessee shall be liable for payment of taxes directly and failure to do so shall make him an assessee-in-default.

The following table explains the consequences more clearly.

(i) has furnished his return of income under section 139.

(ii) has taken into account such sum for computing income in such return of income, and

(iii) has paid the tax due on the income declared by him in such return of income,

And furnishes a certificate to this effect from an accountant in such form as may be prescribed. In that case, the employer shall be liable to pay interest as stated in the table above only from the date on which such tax was deductible to the date of furnishing of return of income by the employee.

ESOPs become an option to create a huge corpus. They work as a generational wealth and create true personal financial treasure for employees.

Image from : https://unsplash.com/@homajob