Traditionally the concept of retirement refers to an age when one chooses not to work permanently. In India the accepted age of retirement is 60 in case of government bodies and 58 for private entities mostly. However, depending on one’s choice and circumstances, one may continue to work for a few years after this defined age of retirement, or may also decide to retire early. Old age is the time when we prefer not to worry about many things, and just cherish the remaining years of life happily.

To live a comfortable life an individual does a lot of hard work. He/she spends their entire life to reach their goals, both financially and otherwise. Receiving good education, getting a nice job, having one’s own house and car, getting married and having a family, and last but not the least taking care of children’s education- the whole life cycle spins around this order. What happens when all the targets are achieved? When nothing is left to be done? It is time to take care of your post retirement life and health.

Throughout the lifetime, a habit should be cultivated to save, save for your future when there shall be no monthly income. It is great to have saved via PPF/EPF accounts or gratuity or any other annuity plans. If you are eligible for a pension, that will help you in managing your monthly expenses better. Retirement needs proper planning and should not be left out while taking care of many other targets when you are still young.

Wise step is to start early. Decide how much you need at the end of your jobspan based on your current needs. Saving a percentage of your income now will save you from many unforeseen situations that you may have to face later. Remember that inflation will also add to the amount of expenses.

It is important to understand both the importance of retirement planning and also how to do it. Here is an overview of the retirement plan one could possibly make. Excel sheet

In this process, identify the retirement income goals. Make an estimate of expenses and construct a saving plan. The actions required to implement the decision will follow according to the plan. Consider all the matters by giving equal weightage to them. There are a few retirement products that you should consider.

What are the retirement products? The planning and investment should start while you are young and earning. That is called the accumulation period. Distribution phase will start once you retire.

There are a few investment options which help you in setting aside a lump sum so that you can get regular income in post retirement years. Following are few of the retirement products which you may consider:

- NPS- National Pension Scheme is considered to be a perfect retirement product in our country. The fund managers of this scheme can take exposure to equity and equity related instruments. It is available for government and private sector employees. NPS too is an EEE instrument where the entire corpus escapes tax at maturity and the entire pension withdrawal amount is tax free.

- EPF-Employees Provident Fund is the most popular retirement saving instrument in India. The current rate of return from EPF is fixed at 8.5% for FY 2020-21. The EPF ensures that every employee has only one EPF account. It helps in saving money for the long run. Deductions are made on a monthly basis from the employee’s salary and a huge amount of money is saved over a long period. It helps an employee financially during an emergency.

- Equities-The returns provided by equity related instruments like stocks and mutual funds are comparatively more than any other options. But you have to pick products for the long term and you should stick to your plans. If something goes wrong, then the investment strategy can be changed. Mutual funds with monthly SIPs are also a good option. The risk appetite of each individual is different. Those who are risk averse would not like to invest in any market linked instruments.

- Exchange Traded Funds-If you know how they work, consider them as a part of your retirement portfolio. Their simplicity and low fees make them perfect for retirement accounts. Passively managed funds have lower fees and could be an option to invest in.

- Bonds-For both younger investors and close to retirement investors, bonds are a good choice. Those who seek stable return may consider them. However, type of bond, interest it pays, lock-in period and risk tolerance are a few factors that affect the bond investment option.

- Monthly Income Schemes: Various mutual funds provide regular income in the form of funds. Post office is also one of them. You can invest a certain amount and the corpus gives you monthly income. Post office monthly income plan gives interest @ 8.5% and maturity period is 5 years.

- SCSS: This is a kind of post retirement product which is the safest for senior citizens. It yields interest @ 7.4% with a maturity period of 5 years. The account under this scheme can be opened in a bank or a post office.

- Pension plans: Insurance companies as well as mutual funds offer such plans. Just like SCSS or MIS you can earn monthly income by investing a lump sum amount.

- Liquid Funds and FDs: All the above options do not guarantee any liquidity. Senior citizens need to keep aside a particular sum of money in case of emergency. At the same time it should fetch good returns. Liquid funds or fixed deposits of different kinds allow such benefits. Liquid funds are tax efficient too.

The National Pension System is one of the best options available for retirees. NPS is preferred by many and is supported by numerous advantages.

Why NPS?

NPS is popular due to its tax benefits. The investments are easy to make. The major concern for senior citizens is the safety of their funds and a fixed-handsome income. Since NPS is regulated by PFRDA under the Ministry of Finance, it is a worry free investment. Previously NPS was available only for government employees, now it is open to all Indian citizens as well as NRIs. Furthermore,

- It is easy to open an account if you want to contribute towards NPS. Both online and offline procedures are very friendly. Public and private financial service providers can help you open an account. Online process is also simple and quick. You need not go out during the current COVID situation and just open an account comfortably while working from home.

- There are two types of accounts, Tier-1 and Tier-2. Whichever you choose, the minimum deposit is only Rs. 1000 per annum. As against this, the returns provided by NPS are much higher. They fetch as high as 15.86% for a period of five years. It is very cheap considering the enrollment, transaction and maintenance charges.

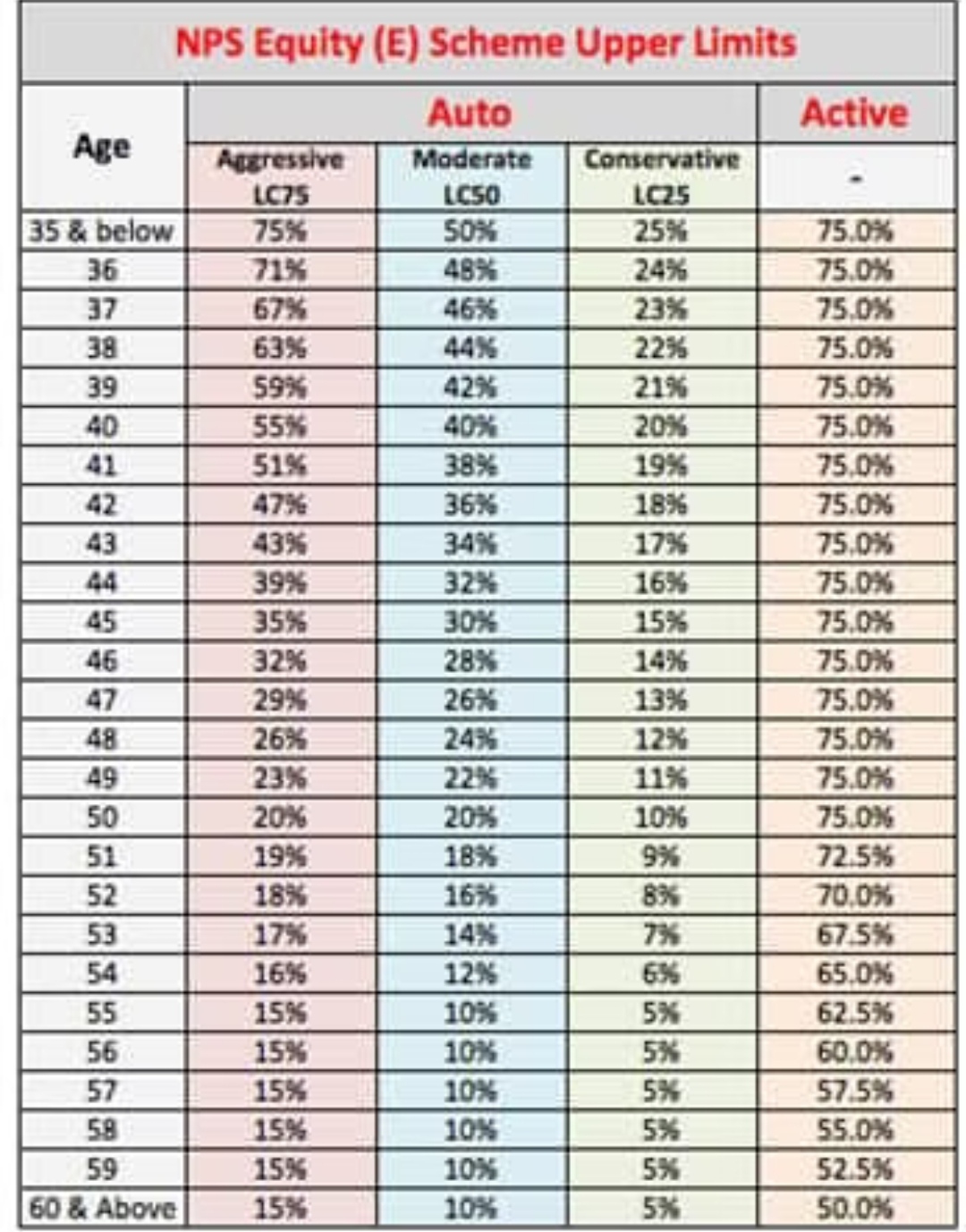

- Qualified fund managers explain the information as the system offers flexibility to choose between asset classes. You can allocate your funds as per your risk appetite. There is an Active choice option where you can invest in equity, corporate bonds, government securities and alternative assets. It allows an equity ratio to be as high as 75% of your investment amount. The Auto choice gives you an option to reduce risk as your age increases. The share of equity and Corporate Debt decrease with age. After the age of 50, the equity portion decreases at 2.5% p.a. And after 60 it becomes 50%.

- NPS Tax Treatment that makes it distinctive-

- Tax Benefits on Investment: The most important point that makes NPS popular is the tax advantages it offers. Contribution up to Rs.50,000 is exempt under section 80CCD(1B) in addition to the one made upto a maximum of Rs. 1,50,000 under section 80C. Employers can also contribute, making it an exempt contribution again(Section 80CCD(2) up to 10% the basic salary of an employee.

- Tax Benefits on Returns: Returns earned on NPS investments are entirely tax exempt.

- Tax Benefits on Maturity: The government has extended the benefits on the entire 60% withdrawn as lump sum at the time of maturity from FY 2020-21 as announced in Union Budget 2019. Thus,NPS becomes a complete EEE investment product.

What is the difference between Active choice and Auto choice and how is it made?

There are two ways to invest in the NPS-A default auto choice for those who find it difficult to decide. It is a passive approach. Whereas an active choice is for the subscribers who want to manage or control their investments. You become the designer of your own portfolio, depending upon how much risk you want to take.

The subscriber chooses the Pension Fund Manager as well as scheme preference while registering in CRA under NPS. You have to first select the PFM and then select any one of the Investment options, namely Active or Auto.

The following are the listed Pension Fund Managers(PFMs) under NPS:

- Birla Sunlife Pension Management Limited.

- HDFC Pension Funds Management Company Ltd.

- ICICI Prudential Pension Funds Management Company Limited

- Kotak Mahindra Pension Fund Limited

- LIC Pension Fund Limited

- Reliance Capital Pension Fund Limited

- SBI Pension Funds Private Limited

- UTI Retirement Solutions Limited

The four asset classes are described in the following chart according to their composition-

Active Choice

After selecting the PFM, choose from four available asset classes, you can choose and adjust them according to your preference. Provide your choice of Asset Class as well as percentage allocation to be done in each scheme of the PFM.

- The cap on equity investments gets decreased once the subscriber reaches age 50.

- Upto 50 years of age, the maximum permitted Equity Investment is 75% of the total asset allocation.

- From 51 years and above, maximum permitted Equity Investment will be as per the allocation matrix provided below. The tapering off of equity allocation will be carried out as per the matrix on date of birth of the subscriber.

- The overall asset class allocation under the Active Choice option should be equal to 100%.

- Percentage contribution value cannot exceed 5% for Alternative Investment Funds.

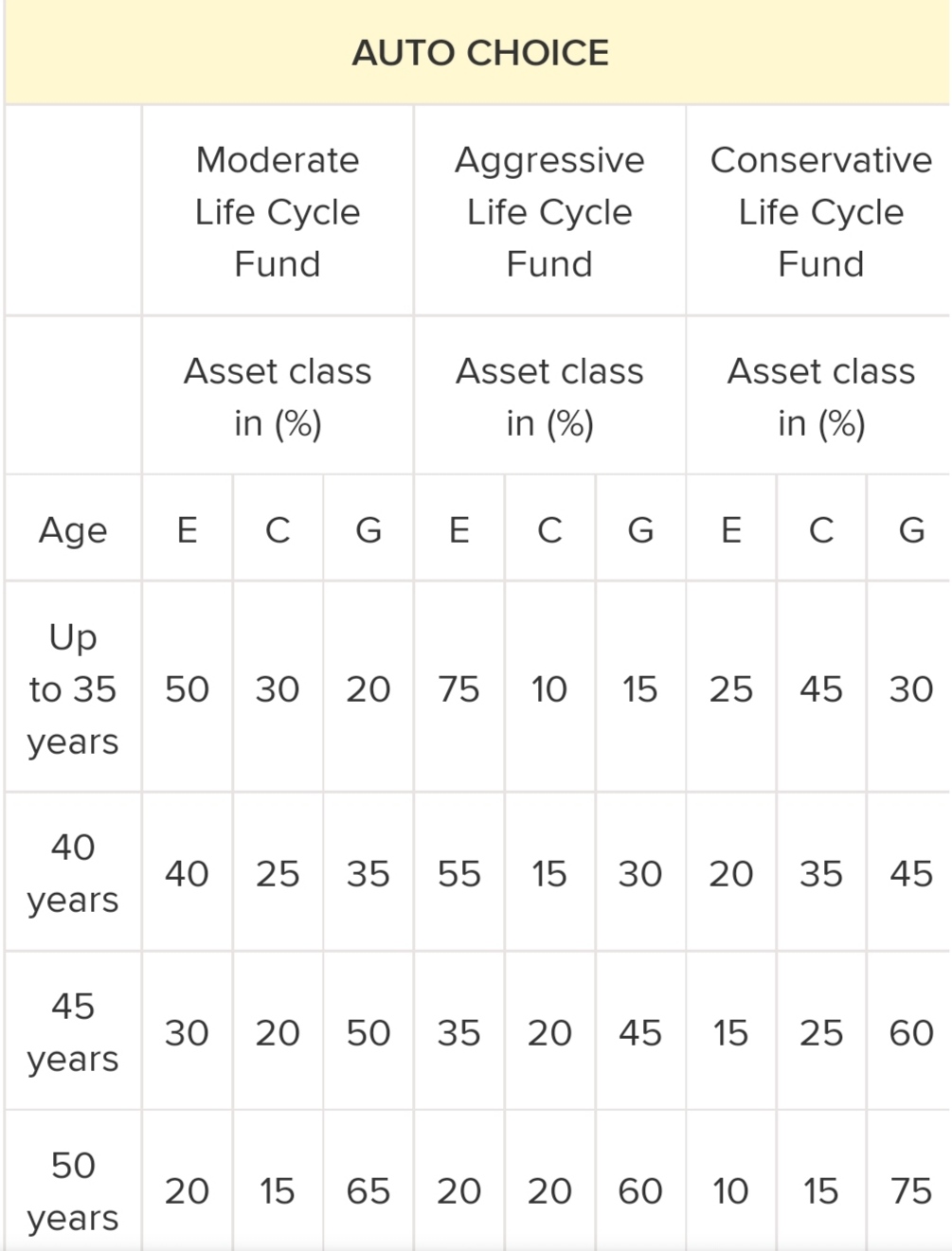

Auto Choice

NPS gives the flexibility to opt for an automatic allocation of your portfolio. As per the age of the subscriber,he/she has to select a Pension Fund Manager and the funds will be invested as per the Life cycle fund matrix.The following chart shows the allocation of each asset class depending upon the age group of the subscriber.

There are three life-cycle funds to choose from-

- Conservative Life Cycle Fund(LC 25):

- Moderate Life Cycle Fund (LC 50): Under this option the equity exposure is limited to a maximum of 50%

- Aggressive Life Cycle Fund(LC 75): In this option, the equity allocation is allowed upto 75%.

The table below will show you the exact percentage allocation of the three asset classes under both the Active and Auto Choice options as per your age.

Types of NPS Accounts:

- Tier I- This account is a non-withdrawable permanent retirement account. At the age of 60, 40% must be used to buy an annuity and 60% of the corpus is tax-free. It avails a tax deduction u/s 80C up to a contribution of Rs.1,50,000 per annum and in addition to this Rs.50,000 per annum u/s 80CCD(1B).

- Tier II- It is a voluntary retirement-cum-savings account. From FY 2020-21, tax benefits can be claimed on Tier-II accounts contributed but with a lock-in period of 3 years. It is now at par with ELSS.

How to open an NPS account?

Both online and offline options are available. You can go to your nearest NPS Point-of-Presence if you want to open an NPS account offline or in person which is a designated branch of your bank. The full list of NPS PoPs is here. If you have an Aadhar Card,PAN Card,and bank account you can open an NPS account online at enps.nsdl.com or enps.kfintech.com. These are the portals of the Central Record Keeping Agencies or CRAs in the NPS.

Using either of the online or offline options, you can make contributions, change key details, change fund managers and initiate withdrawals online at enps.nsdl.com.

To login your NPS Account, you are required to have an official NPS account and PRAN-Permanent Retirement Account Number which is a unique 12 digit number that identifies those individuals who have registered themselves under the National Pension Scheme(NPS). Since it is a must for both the central and state government employees, the registration can be done for PRAN with NSDL.

NPS Login via NSDL NPS Portal

Login to http://www.npscra.nsdl.co.in/

- Now, click on “Open your NPS Account/Contribute Online”

- On the redirected page, select “Login with PRAN/IPIN”

- Insert your PRAN and Password

- Click on “Proceed” and Submit to view your E-NPS account

*If you are accessing your account for the first time, follow the steps mentioned below and create a new password-

- Go to https://npscra.nsdl.co.in/

- Select “Open your NPS Account/Contribute Online”

- Click on “Login with PRAN/IPIN” on the page

- Now, on the log-in screen, click “Password for e-NPS”

- Generate your new password

- Insert all the required details- PRAN, Date of Birth, New Password

- Confirm Password and Click on “Submit”

- An OTP will be sent to your registered mobile number. Enter the OTP to confirm your new password

NPS Login via Karvy NPS Portal

- Go to https://enps.kfintech.com/login/login/

- Click on “Existing Subscriber Login”

- Enter your PRAN and Password to access the e-NPS Portal

E-NPS Portal is accessible through internet banking websites of different Banks as well. You can log-in to your respective banking website and navigate to the NPS page to view all the account details.

How to check NPS balance online?

Check the current value of your NPS investment online by following the below mentioned steps:

- Visit the NPS login page on NSDL website

- Enter your PRAN as user id and password to login to your NPS account

- Once you have successfully logged in, click on the ‘Transaction Statement’ tab

- You can download both of your ‘Holding Statement’ as well as ‘Transaction Statement’ by clicking on either option from the drop down menu.

NPS Contribution

NPS Tier I-The minimum initial contribution is Rs 500. Whereas the minimum annual contribution to your NPS Tier I account is Rs 1,000. There is no maximum annual contribution.

NPS Tier II-the minimum initial contribution is Rs 1,000. There is no minimum or maximum annual contribution. The minimum amount per contribution is Rs 250.

How to make withdrawal from an NPS account?

As per the latest rules, the subscriber can withdraw the corpus amount from the NPS account if the corpus is up to Rs. 5 lakh. Additionally the subscriber can withdraw the entire accumulated lump sum accumulated on maturity without having to buy compulsorily. (The provisions required that the person can withdraw up to 60 percent of the amount and the rest of 40% is used to buy an annuity plan.)The limit on premature lump-sum was Rs. 1 lakh, which is now extended upto Rs. 2.5 lakh.

The maximum age has been increased from 65 to 70 and the exit age limit stands at 75 years. Those who are above 65 years of age can enrol under the scheme and get the benefits. The subscriber can defer the annuity purchase for upto three years from the time they turn 60 years old or attain the age of superannuation. In a case where the accumulated pension wealth of the subscriber is more than Rs. 2.5 lakh but his/her age is less than the minimum age required for getting an annuity plan will continue to be subscribed to the scheme until he or she attains the age of eligibility for buying annuity. But they can withdraw the entire amount without buying any annuity if the accumulated pension wealth is equal to or less than Rs. 2.5 lakh in that case.

If the subscriber attains the age of 60 years or superannuates in accordance with the service rules applicable to him/her, at least 40 percent of the accumulated pension wealth shall be mandatorily used for purchase of annuity providing for a monthly or any other periodical pension and the balance will be paid to the subscriber in lump sum. But where he/she wants to continue beyond the age of 60 years of the age of superannuation, a written form needs to be given as may be specified at least 15 days prior to the age of attaining the age of 60 years or age of superannuation. The contribution can be continued till 70 years of age and the account will be shifted from the government sector to All citizens including the corporate sector.

In the case of the subscriber’s death the amount can be withdrawn in its entirety as a lump sum and there would be no option to purchase annuity or monthly pension after the death of the subscriber.

A partial withdrawal is allowed subject to reasons like higher education and marriage of children, for the purchase/construction of a residential house/flat in her or her own name or in a joint name with his or her legally wedded spouse. But if an ancestral house/flat is already owned, no such withdrawal can be made. For treatment of specified illnesses suffered by subscriber, his/her legally wedded spouse, children including a legally adopted child and dependent parents. Maximum of three withdrawals are permitted during the entire tenure of subscription.

If the subscriber wants to exit from the scheme, he/she has to submit a completely filled withdrawal application form along with required documents to the POP-SP. The POP-SP will forward the form to the CRA:NSDL e-Governance Infrastructure Limited, after authenticating the documents.

The subscriber’s claim will be registered and CRA will forward the application form. The CRA also assists subscribers by providing necessary information about required documents. Once the documents are received and verified, the application will be processed and CRA will settle the account.

The amount of pension that you will get in the NPS

It all depends on the performance of your NPS funds. As your contributions are invested in assets like equity or debt and earn returns, the corpus is thus expected to steadily grow over time.

When you hit the age of 60, you can use the accumulated corpus to buy an annuity (monthly pension). The actual pension you get depends on the corpus size and the prevailing annuity rates.

[…] NPS or National Pension Scheme is a voluntary retirement savings scheme. It encourages citizens to cultivate a habit of systematic savings while they are working. The individual savings thus pooled into a pension fund are invested in diversified portfolios comprising Government Bonds, Bills, Corporate Debentures and Shares. The employees of the corporate entities, who are Indian citizens and are enrolled by the employer between the age of 18-60 are eligible to subscribe under NPS. […]