Retirement planning is a very significant matter and plays a major role in an individual’s financial goals. It needs a dedicated and continuous effort to save and create a corpus for your retirement life. This becomes possible only through schemes specially meant for such purposes with a disciplined approach.

Employees who joined government service before 1st April 2004 were eligible for pension. The employees used to get fifty per cent of their last drawn salary together with Dearness Allowance to combat the effects of inflation. The private sector employees do not have any such benefits and they have to depend on their own savings to build a retirement corpus. For that Employees’ Provident Fund account and National Pension Scheme are widely relied upon. A private sector employee can create a regular pension-like source of income just like a government employee.

Among the most popular products available for retirement planning are The National Pension Scheme and the Employees’ Provident Fund. An establishment employing more than 20 employees is required to contribute towards EPF. The employees whose basic salary is more than the threshold limit can also contribute.

NPS or National Pension Scheme is a voluntary retirement savings scheme. It encourages citizens to cultivate a habit of systematic savings while they are working. The individual savings thus pooled into a pension fund are invested in diversified portfolios comprising Government Bonds, Bills, Corporate Debentures and Shares. The employees of the corporate entities, who are Indian citizens and are enrolled by the employer between the age of 18-60 are eligible to subscribe under NPS.

EPF stands for Employees Provident Funds and it is a non-constitutional body promoting employees to save funds for retirement. It covers both the Indian as well as international workers from countries with whom the EPF organisation has signed bilateral agreements.

It is mandatory for the employees and the employers to contribute towards EPF. Each of them makes a 12% contribution of the employees’ basic salary and dearness allowance towards the fund. EPF has its unique benefits.

As both the schemes focus on savings for retirement purposes, several employees choose either or both of them. The advantages of each of the above schemes are distinct and make employees choose between them. We will discuss NPS and EPF along with their features to make readers better understand the difference between them, thereby helping them make better choices for themselves.

NPS or EPF-A comparison

Majority of salaried individuals have access to both EPF and NPS. The sole purpose of these schemes is to create a retirement corpus for the contributor. Hence, both of them do not allow early withdrawals. But that works as an advantage for the employees as the amount contributed by them gets compounded and they can use this fund after they retire as a replacement for their regular income.

- Both the schemes offer tax incentives. Under section 80C of the Income Tax Act, a maximum deduction of up to Rs. 1.5 lakh is allowed for the amount invested. In the case of NPS, you get an additional deduction of Rs. 50,000 under section 80CCD(1B). This could work better for those who fall into the highest tax bracket of 30%. The net returns on NPS after considering tax savings on it will be much higher.

- EPF offers defined benefits. EPFprovides returns every year and those are guaranteed by the government of India. The lump-sum amount is given to the employee upon him reaching his retirement age. Whereas in the case of NPS, money is invested in equity and debt markets. So you definitely save money and contribute it towards securing your future, but the returns depend upon market functionality. NPS also earns enough to give you handsome returns.

- EPF is meant solely for salaried individuals but NPS can be used by any individual irrespective of their job or kind of work. It entails benefits to all who want to subscribe to it. NPS is more flexible and you can contribute as much as you want subject to a cap of a maximum of 75% towards equity allocation. But if you do not withdraw from EPF, then the fund gets accumulated and turns into a huge corpus.

- The objective of both the schemes though looks similar, but the outcome may be slightly different. EPF is a compulsory contribution made both by the employers and the employees, it helps one to cover his/her monthly expenses after retirement. NPS could earn you better returns to pay your necessary expenses and allows room for other expenses as well.

- Talking about investment contribution, EPF contributions are invested in securities issued by the Central and State governments, PSU bonds and deposits. The contributions made do not have any impact on the contributor’s pension. Despite bond and security yields being flexible, the annual compounding interest on these deposits will be paid to contributors.

In the case of NPS, there are two investment modes, one is an active choice and the other is an automatic choice.

By opting for the latter option, the investor can have up to 50% of their portfolio in equity and the rest in low or medium return, fixed income products. The auto choice option works taking into consideration the contributor’s age. If the contributor is a government employee, then the equity exposure is limited to 15% in a Tier 1 account.

- EPF contributions come from your employer too. About 8.33% of the employer’s monthly contribution will be redirected to the Employee Pension Scheme (EPS). A retired person who had continuous employment for the last 10 years is eligible to withdraw 100% of the EPS account balance. As per the EPFO website, the maximum salary considered for the calculation is Rs. 15,000, effective from 10th June 2008.

Those who like to contribute more can opt for NPS as it allows additional tax benefits and has no limit on contributions. One may invest higher amounts to meet his/her retirement goals. 60% of the NPS fund is tax-free on maturity. EPF maturity proceeds are tax-free subject to interest earned on the annual contributions made in excess of Rs. 2.5 lakh.

The table below shows the differences between the two.

| Criteria | EPF | NPS |

| Nature of contribution | Mandatory for employees earning basic pay less than Rs. 15,000 and voluntary for others | Voluntary |

| Who is allowed to invest | Salaried individuals | Any citizen irrespective of their source of income |

| Withdrawals | Partial withdrawal allowed for specific reasons like medical emergencies etc. | 25% of the fund amount can be withdrawn subject to a lock-in period of three years after subscription for predefined purposes |

| Minimum Investment | 12% of salary per month | Minimum of Rs. 500 for Tier-I and a minimum of Rs. 1000 for Tier-II |

| Expected rate of return | Approximately 8-8.7% p.a | Market linked returns, but they can be in the range of 9-12% |

| Risks involved | Guaranteed returns by government and are safer. | NPS is a market-linked scheme and hence is subject to market risks. |

| Tax Benefits | Employee contribution of up to Rs. 1.50 lakh is eligible for tax benefits. Interests up to Rs. 2.5 lakh and maturity proceeds are tax-exempt. | Anyone who contributes is eligible for tax deduction up to Rs. 1.50 lakh. An additional deduction of Rs. 50,000 is available. Maturity proceeds are tax-exempt for up to 60% of the total amount. The remaining 40% is taxable and gets converted into an annuity. |

| The choice to invest as per your preference | Is not given | An investor can choose from equity, corporate debt, G-sec and alternative asset classes. |

Drawbacks of EPF

There are a few drawbacks of EPF like it doesn’t give the choice to choose your portfolio of equity investments. It is suitable for those investors who are risk-averse.

If you’re ready to invest more in equity, such an option is not available in the case of EPF. Moreover, the EPF interest rate has been reduced. It was 11% in 2001 as compared to 8.1% in 2022. Those who are in the initial period of their job/career will not benefit if rates keep falling.

NPS is open for all, whereas EPF has limited access, as the name suggests, it is available to employees only.NPS is ideal if you want higher returns in the long run.

Drawbacks of NPS

If we talk about the disadvantages of NPS, the biggest concern is tax treatment at the time of retirement. Only 60% of the corpus can be withdrawn which is also tax-exempt. The rest of the corpus is invested in annuity and is also subject to tax. An investor cannot invest this amount though there are options like mutual funds to invest in. The income from the annuity is taxable depending upon your tax slabs. Plus, one cannot have a clear cut idea regarding how much annuity is needed as per an individual’s unique requirements. So investing 40% of the corpus at the time of retirement again calls for a fresh investment strategy.

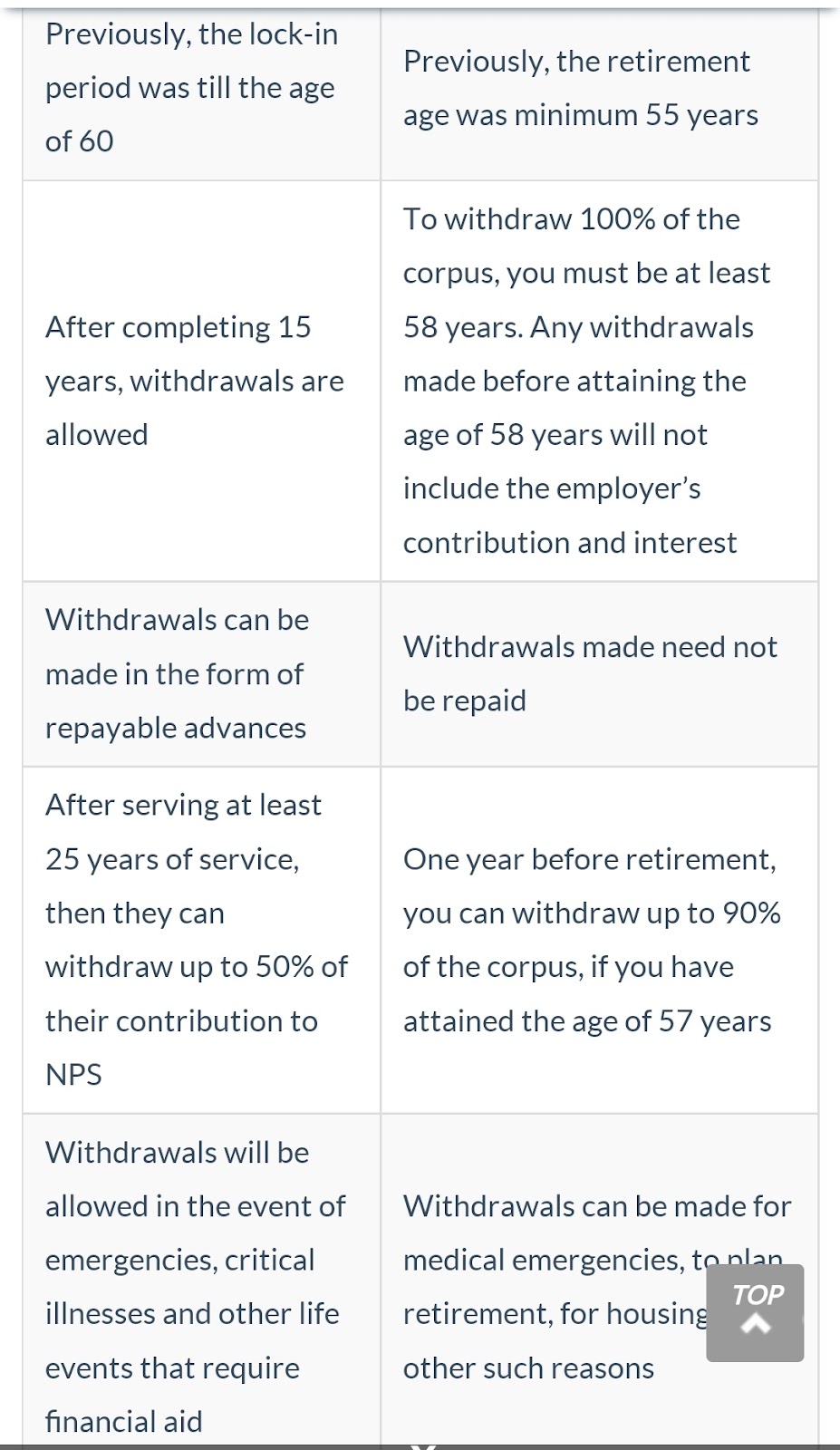

Withdrawals

EPF allows withdrawals subject to the condition that the contributor cannot withdraw more than six times their annual pay for medical treatment. To repay a home loan, a withdrawal of up to 90% of the corpus if the house is registered in his name or her name or held jointly. At least 3 years of completed service is required.

Similarly, to acquire a site or block of property it is allowed up to 24 times of your annual wage only after completing 5 years of service, 12 times of annual pay to repair and remodel the house after 5 years of total service and 50% of the contributions can be withdrawn up to three times for marriage or schooling subject to 7 years of service.

The withdrawal is allowed for medical treatment of self, spouse, children and parents. There is no minimum lock-in period for this type of withdrawal. A person can withdraw the entire corpus after completing 58 years of age. 90% of the EPF balance can be withdrawn after the age of 54 years.

NPS allows the subscriber to withdraw only thrice during the tenure of the entire subscription. There must be a gap of 5 years in between these withdrawals. Only 25% of the amount can be withdrawn. Minimum three years subscription is necessary to be eligible for partial withdrawal. The withdrawal is permitted for the education of children, marriage expenses, house construction and medical emergencies. There are different rules for government sector subscribers, subscribers who work for the government but take voluntary retirement, corporate sector employees and citizens on retirement and their voluntary exit, and death in all the above cases.

An aggregate contribution in excess of Rs. 7,50,000 to EPF, NPS and Superannuation Fund is taxable in the hands of the employee.

The difference between EPF and NPS withdrawal rules is shown in the following table for NPS (left) and EPF (Right)

Topping up your EPF with NPS

EPF might not be sufficient for many salaried individuals. If the rate of return is less, say somewhere around 7% p.a, then you should look for other schemes. Furthermore, if the salary increment is more than 5%, then your last drawn salary will be a higher amount, prompting you to want the same level of income after you stop working. In that situation again, you have to contribute more to keep your monthly income at the same level. You can choose NPS in that case.

NPS is comparatively new as it has been introduced in the last decade. The additional tax saving of Rs. 50,000 could be of much help to those taxpayers who fall into the higher tax slab. It is good to have a higher allocation to equity via NPS.

You may also like to invest in a Voluntary Provident Fund. In order to have a combined benefit of fixed income and tax benefits, VPF could be of help. It is a long term debt investment option, yielding a good interest rate and also offers tax benefits.

Nomination and other things

EPS and NPS both require a nominee so that the nominated family member can get the benefits of the scheme. You can nominate anyone for your EPF account. EPF gives a fixed income to you upon your retirement. When you withdraw from EPF at the time of your retirement, you get benefits of both the EPS and the EPF.

Both the schemes allow nomination in favour of one or more persons belonging to the subscriber’s family if he/she has a family at the time of making a nomination. But the subscriber cannot nominate a person not belonging to his family as it is considered to be invalid. A fresh nomination is required for the subscriber when he/she gets married. Any prior nomination made before such marriage will be deemed to be invalid.

EPF and NPS also allow nominating any person only in a case where the subscriber does not have a family. If the subscriber later acquires a family, the former nomination becomes invalid. There are various other nomination rules in the case of NPS that one must study before subscribing to it.

EPS and NPS together can earn you a government pension

| Basic salary at age 25 years | Rs 15000 | Rs 15000 | Rs 15000 | Rs 25000 | Rs 25000 | Rs 25000 |

| Annual growth in salary | 5% | 8% | 10% | 5% | 8% | 10% |

| Basic salary at the age 60 years | Rs 82,740 | Rs 2,21,780 | Rs 4,21,537 | Rs 1,37,900 | Rs 3,69,634 | Rs 7,02,561 |

| Desired starting pension* | Rs 41,370 | Rs 1,10,890 | Rs 2,10,768 | 68950 | 184817 | 351280 |

| Corpus needed to last 30 years after retirement factoring inflation** | Rs 1.15 crore | Rs 3.08 crore | Rs 5.85 crore | Rs 1.91 crore | Rs 5.13 core | Rs 9.75 crore |

| EPF corpus built during employment | Rs 1.12 crore | Rs 1.89 core | Rs 2.73 crore | Rs 2.05 crore | Rs 3.33 crore | Rs 4.73 crore |

| Deficit for inflation proof pension | NA | Rs 1.19 crore | Rs 3.12 crore | NA | Rs 1.80 crore | Rs 5.02 crore |

| Monthly NPS contribution needed at the beginning of the job*** | NA | Rs 1,762 | Rs 3,382 | NA | Rs 2,665 | Rs 5,441 |

The following assumptions have been made while preparing the above table-

1. Annual inflation is 5%.

2. EPF contribution is 24% of basic salary minus a deduction of Rs. 1250 for EPS.

3. EPF’s annual rate of return is 8%.

4. Return on corpus during retirement years 7%.

*Half of the basic salary at retirement, ** after retiring at the age of 60 years a monthly pension is given which includes a part of corpus and return earned on a corpus that increases each year to combat the inflation of 5% for a period of 30 years.

***NPS Contribution grows annually in the same proportion as the rise in salary, annual return on NPS contribution is 9%.

Whenever you make any calculations for the future, do not forget to provide the inflation factor. Saving for retirement should take care of inflation by raising the regular income constantly. The government pension is inflation-adjusted and they increase with the pay commission. But in the case when you have set up your own plans, you have to take care of such factors yourself.

To live a retirement life with sustainable income needs a dedicated approach to creating one. You should build a corpus while you are working and maintain it. You need to have a disciplined approach by regularly investing every month. Avoid temptations to use the fund thus created. Alternatively, you may decide to have a well-managed portfolio of equity funds or a combination of various mutual funds along with other fixed income generating debt and other instruments. But in that case, you have to closely watch them and take all the decisions very diligently, as the retirement corpus is a very important part of your financial planning.

It depends upon an individual’s goals and the choice of whether to go for EPF or NPS or both. NPS is riskier than EPF as it is market-linked. But it allows you to choose from a variety of investment options. EPF returns are guaranteed as well as tax-free. NPS gives you a slightly higher return on your investment if you are able to take risks.

Now let’s study a practical example. Suppose a salaried person is earning Rs.30,000 per month. The employee’s age is 30 years and the contribution to EPF is 12%. (The employer also contributes 12% of this amount towards the fund.) Considering an increase in salary at 7% annually and the rate of interest earned on this contribution at 8.5%, the individual will be able to get an accumulated fund of Rs. 2,02,65,724 at the time of retirement. It is assumed that there have been no withdrawals made during this entire period.

Similarly, if we do a case study of NPS contributions made by an individual, we can know about the outcome at the end of a particular period. A person invests Rs. 5000 every month and starts contributing at the age of 30 years. He earns returns at the rate of 11%. He will invest an amount of Rs. 18,00,000 until the time he reaches his retirement age of 60 years. This contribution will grow by 10% every year and his annuity will be 40% of the total corpus. The annuity amount will earn interest at 7%. He will receive a total of Rs. 3,75,19,317 as maturity amount. Out of which Rs. 1,50,07,727 shall be his annuity. And the rest is the lump sum value of Rs. 2,25,11,590.

You can use EPS and NPS calculators available online to compare the outcome of both the schemes by putting the amount of your contribution and other particulars. By using both EPF and NPS carefully, you can create a substantial amount of corpus by the time you retire.

Image from Unsplash – https://unsplash.com/@vladsargu

[…] interest earned on the EPF account shall now have to be bifurcated under two heads. A part of it is not taxable, and the other […]